Describing the blockchain technology for potential applications

The concept of blockchain technology of fundamental principles, and vast potential applications that extend far beyond the realm of finance.

In the digital age, technological innovation for blockchain technology continues to reshape the way we conduct transactions, secure data, and establish trust in the virtual realm.

One technology that has garnered immense attention and promise is blockchain.

In this blog post, we will delve into the concept of blockchain technology, its fundamental principles, and its vast potential applications that extend far beyond the realm of finance.

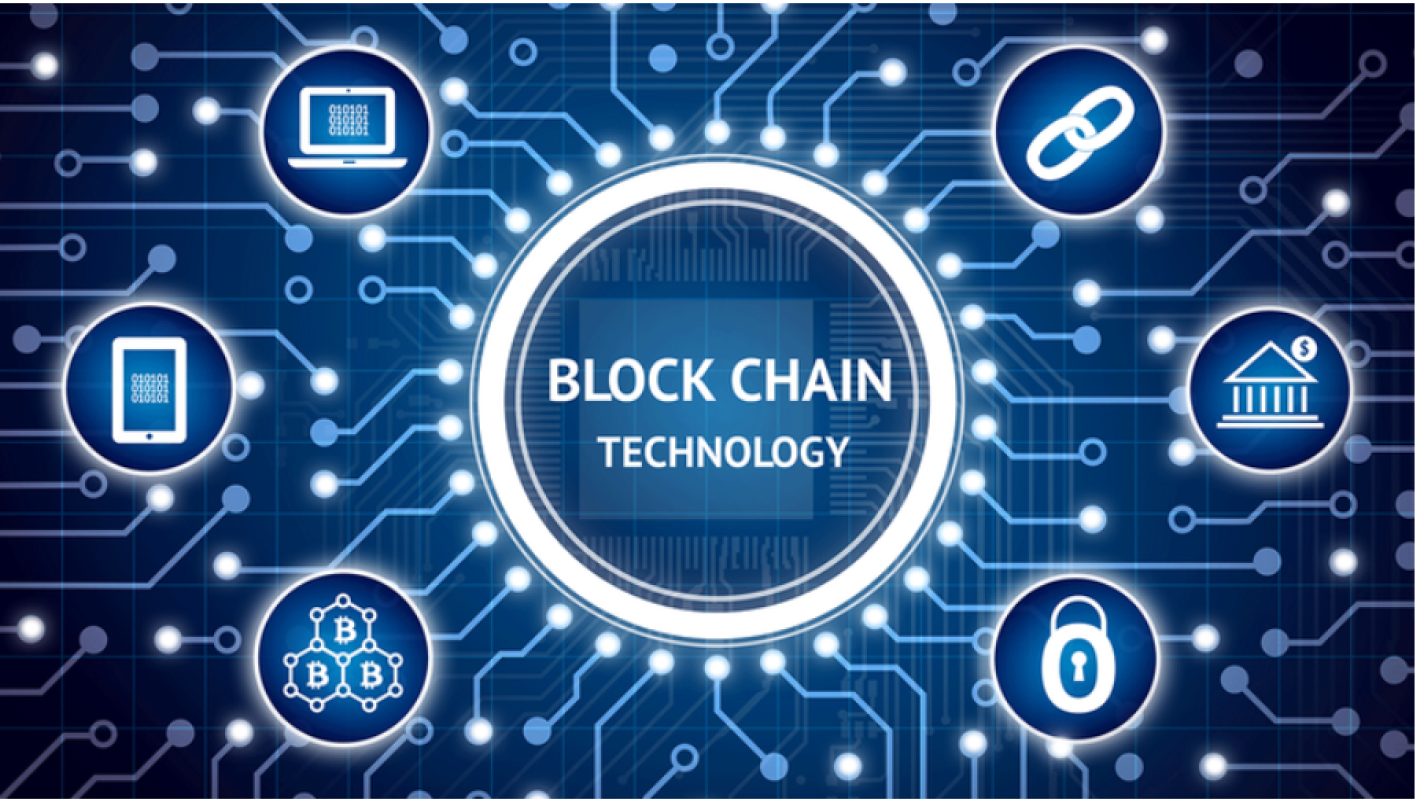

Understanding Blockchain Technology

At its core, a blockchain is a decentralized, distributed ledger that records transactions across a network of computers.

Key Features of Blockchain Technology

- Decentralization: Unlike traditional centralized systems, where a single entity has control over data and transactions, blockchain operates on a decentralized network. This means that no single authority or organization has complete control over the blockchain, making it resistant to censorship and tampering.

- Transparency: Blockchain transactions are transparent and can be viewed by anyone with access to the network. This transparency enhances trust among participants as they can verify transactions independently.

- Security: Blockchain uses cryptographic techniques to secure data and transactions. Once a transaction is recorded in a block and added to the chain, it becomes extremely difficult to alter or delete. This immutability makes blockchain highly secure against fraud and unauthorized changes.

- Trustless Transactions: Blockchain allows for trustless transactions, meaning parties can engage in transactions without needing to trust a third party, such as a bank or intermediary. The technology itself ensures the integrity of transactions.

Potential Applications of Blockchain Technology

- Cryptocurrencies

The most well-known application of blockchain technology is cryptocurrencies. Bitcoin, created in 2009 by an anonymous entity known as Satoshi Nakamoto, was the first cryptocurrency to leverage blockchain as its underlying technology.

They have the potential to disrupt traditional financial systems and provide financial services to the unbanked and underbanked populations worldwide.

- Supply Chain Management

Blockchain can revolutionize supply chain management by providing end-to-end visibility and transparency. This ensures the authenticity of products, reduces counterfeiting, and enhances the traceability of goods.

- Healthcare

Patients can grant permission for healthcare providers to access their data, improving interoperability and reducing administrative overhead.

- Identity Verification

Identity theft and fraud are growing concerns in the digital age. Blockchain offers a robust solution for identity verification. Individuals can control their personal data and share it with trusted entities as needed, reducing the risk of data breaches. Governments and organizations can issue digital IDs that are tamper-proof and easy to verify.

- Voting Systems

Blockchain-based voting systems have the potential to enhance the integrity of elections by providing a secure and transparent platform for voting. This reduces the risk of fraud and manipulation, ensuring the accuracy of election results.

- Intellectual Property and Copyright

Artists, writers, and creators can use blockchain to protect their intellectual property and ensure fair compensation for their work.

- Real Estate

Real estate transactions involve a complex web of paperwork and intermediaries. Blockchain can streamline the process by recording property ownership and transactions on a secure, immutable ledger. This reduces the risk of fraud and simplifies the transfer of property titles.

- Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code.

- Energy Trading

Blockchain can facilitate peer-to-peer energy trading in the emerging field of decentralized energy grids. Producers of renewable energy can sell excess energy directly to consumers, bypassing traditional energy providers. This promotes sustainability and reduces energy costs.

Challenges and Considerations

While blockchain technology offers numerous advantages, it also faces challenges and considerations:

- Scalability: As blockchain networks grow, they must address scalability issues to handle a high volume of transactions efficiently.

- Energy Consumption: Proof-of-work blockchains, like Bitcoin, consume significant amounts of energy. Efforts are underway to develop more environmentally friendly consensus mechanisms.

- Regulation: Governments are still developing regulations for blockchain technology, which can impact its adoption and use cases.

- Interoperability: Ensuring that different blockchains can communicate and work together seamlessly is an ongoing challenge.

- Privacy Concerns: While blockchain provides transparency, it can also raise concerns about data privacy, especially in public blockchains.

Blockchain technology is a groundbreaking innovation with the potential to disrupt a wide range of industries and redefine the way we conduct transactions, secure data, and establish trust.

From cryptocurrencies to supply chain management, healthcare, and beyond, the applications of blockchain are vast and promising.

However, it is crucial to address challenges and regulatory considerations as the technology continues to evolve. As blockchain matures, it will likely play an increasingly integral role in the digital transformation of our society, offering new opportunities and solutions for various sectors and industries.

What's Your Reaction?